Duke Energy’s Junior Debt Offers 5% Yield (DUKH)

By: Ned Piplovic,

Duke Energy Corporation (NYSE: DUK) boasts an impressive history of more than 90 years with dividend distributions, including a recent streak of a dozen consecutive dividend boosts. However, investors who prefer not to wait until the company’s next quarterly dividend payout in May 2017 can take advantage of the company’s junior debt note that will pay its next dividend in mid-April.

While the company’s share price (DUK) is still lingering just slightly above its recent low following the February market sell-off, the debt note’s (DUKH) share price has recovered almost completely and currently trades approximately 1.5% below its January 2018 levels prior to the February market drop.

Thus, investors looking for a quick dividend payout might consider the debt to be a better option at this time, but the share price dip in the company represents a good chance to take a long position in Duke Energy’s stock.

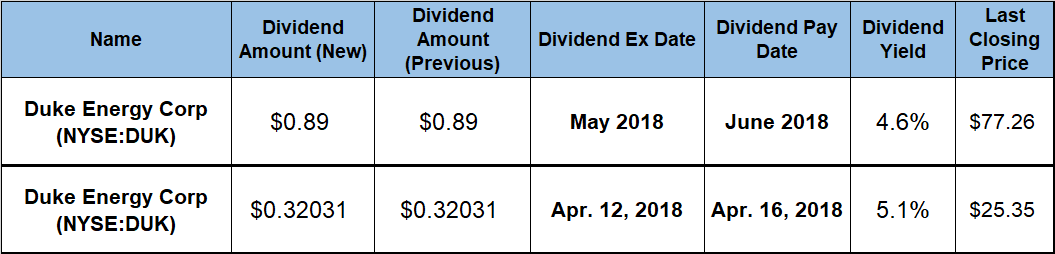

Duke Energy will pay the next dividend installment on its debt note on April 16, 2018, to all its shareholders of record before the next ex-dividend date, which occurs just four days before the pay date on April 12, 2018.

Duke Energy 5.125% Junior Subordinated Debentures (NYSE:DUKH)

Currently headquartered in Charlotte, North Carolina, the Duke Energy Corporation, operates as an energy company through three segments: Electric Utilities and Infrastructure; Gas Utilities and Infrastructure; and Commercial Renewables. The Electric Utilities and Infrastructure segment uses coal, hydroelectric, natural gas, oil, renewable resources and nuclear power to generate and distribute electricity in the Carolinas, Florida and the U.S. Midwest. This segment owns approximately 50,000 megawatts (MW) of generation capacity and serves around 7.5 million retail electric customers in six states. The Gas Utilities and Infrastructure segment owns various pipeline transmission and natural gas storage facilities for distribution of natural gas to nearly 1.5 million customers in the U.S. Southeast. Finally, the Commercial Renewables segment builds, develops and operates wind and solar renewable generation projects. This segment has 21 wind farms and 63 commercial solar farms with a capacity of 2,900 MW across 14 states.

Duke Energy’s Junior Subordinated Debentures are rated Baa2 by Moody’s, the eighth-highest ranking, which means that the debt is subject to moderate credit risk and is considered medium grade. However, investors willing to take on some risk here stand to benefit from a very respectable 5% yield.

The current dividend distribution – which actually is an interest payment – of $0.32021 per share (5% yield) is the same payment amount that the company has been paying for the past 12 consecutive quarters and converts to a $1.28 annualized distribution amount. At these levels, the current 5% yield is just marginally lower than the five-year average yield of 5.1%.

Additionally, DUKH’s current yield is approximately 90% above the 2.6% average yield of the entire Utilities sector and 110% higher than the 2.36% average yield of the Electric Utilities sub-segment. If one counts only dividend-paying companies in the Electric Utilities segment, the average yield increases to 3.64%, but that number is still 38% lower than DUKH’s.

Interested investors should take into consideration the fact that these payments will be taxed at regular tax rates. Remember, DUKH’s payments are actually interest payments, and so are not considered as qualified dividend distributions and, therefore, do not qualify for favored tax rates.

While the share price is still slightly lower than it was 12 months ago, shareholders still received a total return on their investment of 2% over the past year. The three-year total return was 17.6% and the total return over the past five years was 25.6% Unlike the company’s main stock — which regained 17.2% of its losses and is still more than 15% below its 52-week high — the debt note’s share price regained almost 60% of its losses and closed on April 3, 2018 at $25.35, which is less than 5% below its peak price from mid-January 2018.

Dividend increases and dividend decreases, new dividend announcements, dividend suspensions and other dividend changes occur daily. To make sure you don’t miss any important announcements, sign up for our E-mail Alerts. Let us do the hard work of gathering the data and sending the relevant information directly to your inbox.

In addition to E-mail Alerts, you will have access to our powerful dividend research tools. Take a quick video tour of the tools suite.

Related Posts:

Ned Piplovic

Connect with Ned Piplovic

Connect with Ned Piplovic